Bala: Providing financial autonomy to Indian women using kitty parties

Second Prize - Stanford Longevity Design Challenge '24

Area

Interaction Design

Game Design

My Role

Researcher, Strategist,

Prototyper, Tester

Duration

November 2023 - April 2024

Industry

Finance

Women Empowerment

The Problem

The Solution

By integrating financial education into the already existing structure of kitty parties, we create an engaging and supportive environment where women learn crucial financial skills while maintaining the social and fun aspects of these gatherings.

The Approach

How did we uncover a breakthrough in women's financial empowerment and education?

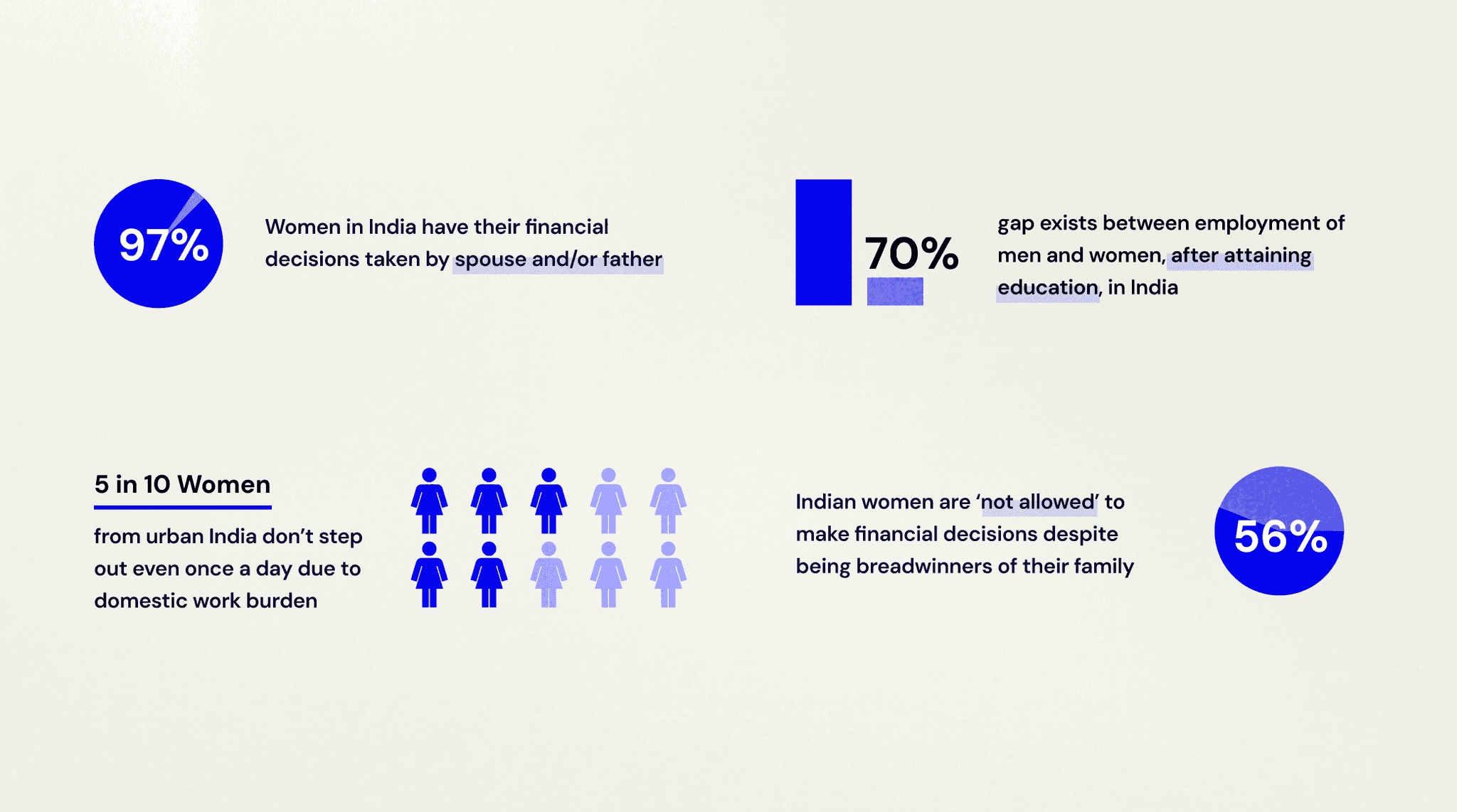

The problems only worsen in India

While the world is showing a positive and progressive trend towards the issue of financial autonomy for women, India is still struggling. There exists numerous barriers which abstain women from let alone exercising their financial rights but even having a say in their finances.

Hearing & engaging directly with the source

We conducted interviews & surveys with 55 women (both employed & non-employed) from diverse socio-economic backgrounds, ranging from low-income to upper-middle-class, and ages 22 to 59.

The women we interviewed also included those working in fields like sociology, economy, fin-tech, and gender study.

Indian women are often confined to household roles, excluded from financial decisions, and left reliant on male relatives. With limited financial education, patriarchal control, and societal pressures, their independence is further restricted. The lack of female role models and supportive networks deepens these challenges.

Diving deeper using cultural probes & more

We conducted three cultural probing activities, designed to gather deeper insights into women's everyday lives, their financial behaviours, and the cultural norms influencing their financial decisions.

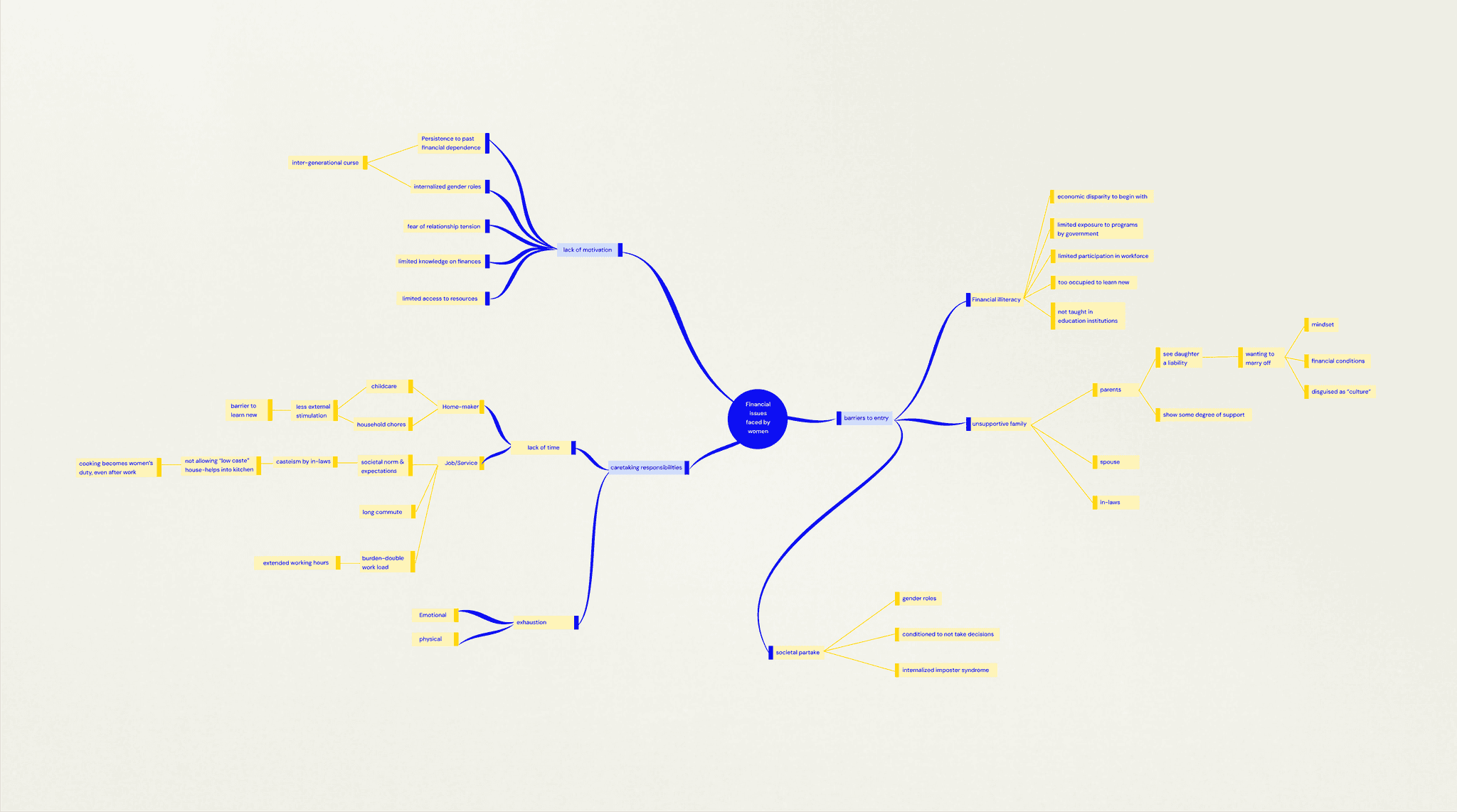

Filtering it all down to actionable insights

Our research uncovered key barriers to women’s financial autonomy, revealing the need for generating interest about financial literacy in them.

These actionable insights guided us to make better targeted interventions to help women overcome societal constraints and take control of their financial futures.

Arriving at the final problem

Addressing this is crucial for fostering financial independence, family well-being, and reducing gender disparities. It ensures long-term security, career opportunities, and a positive impact on psychological well-being, creating a foundation for generational financial literacy.

The road to finding an apt solution

The state of existing services

Despite the emergence of women-centric banking and collaborations with government and private sectors, the effectiveness of these services often falls short of the intended impact.

Kitty Parties - The unlikely star of our research

Kitty parties, a uniquely Indian tradition, blend socialising with finance. Members contribute to a common fund, or 'kitty,' which rotates among them every month, providing each woman with a lump sum for household expenses, education, or entrepreneurial ventures.

Presenting Bala

Bala is a service combining a physical game toolkit and an app, which together help provide financial literacy to Indian women through kitty parties. The game kit's monthly subscription model is derived from the fact that most kitty parties are a monthly recurring meetings. This helps distribute & break down difficult financial concepts into smaller easy to digest chunks.

Facets of the solution

The game kit is divided into two - an active learning card game called Gharkharch (घरख़र्च ) and a set of passive learning games and tools (including a classic card deck - Fintaash (फ़िन ताश), a tote bag, and a puzzle).

Gharkharch - Active Learning Game

Puzzle - One of the Passive Learning Games

Bala App

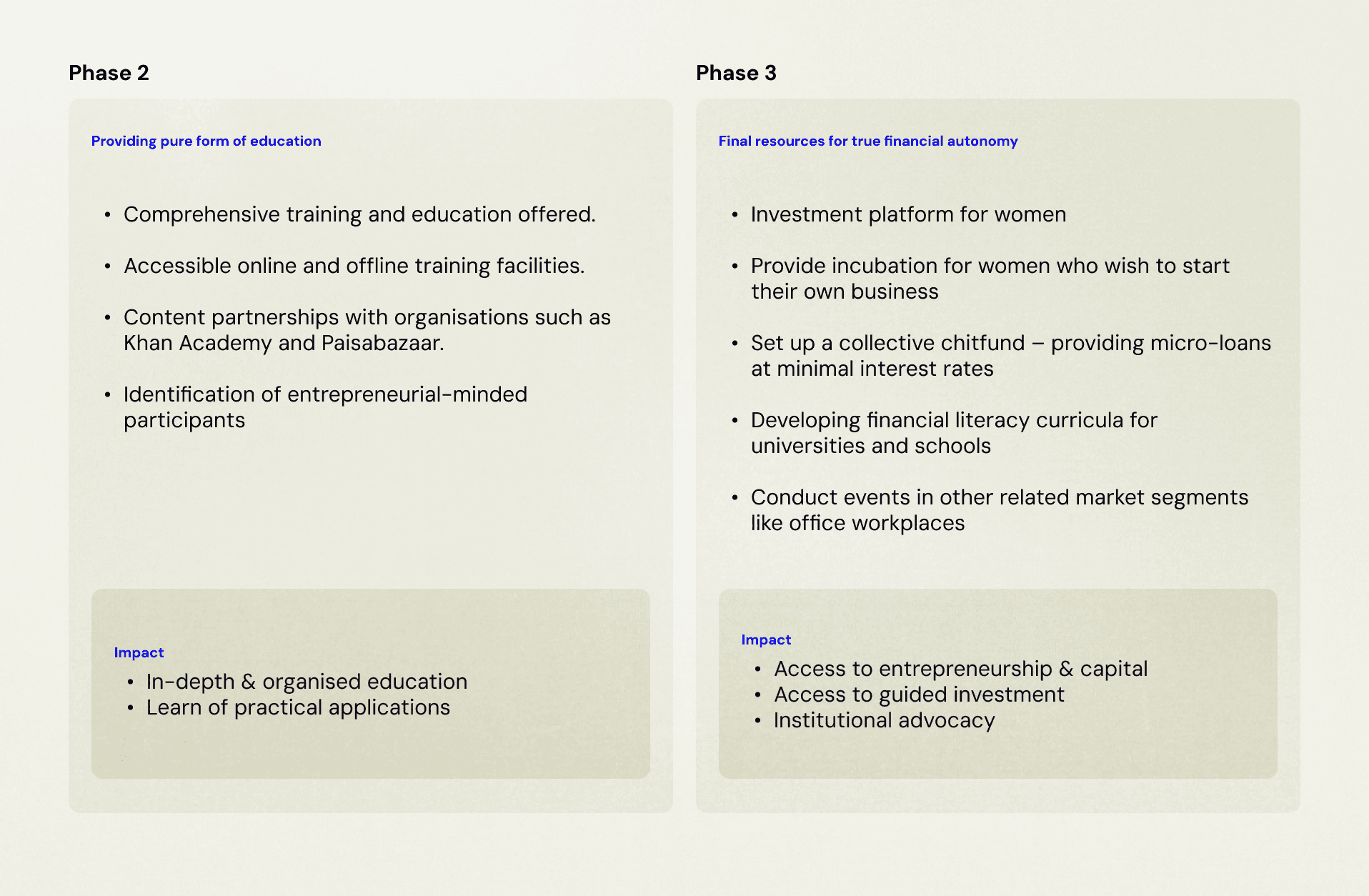

The business model - a Three Phase Plan

The business model is structured into three phases: generating interest in finances among women, equipping them with financial literacy, and ultimately empowering them to apply this knowledge practically to achieve financial autonomy.

What's next?

We are currently actively seeking funding to bring this project to its full potential. With additional resources, we aim to expand its impact, refine key features, and explore new opportunities for growth. Our commitment remains strong, and with the right support, we’re confident this project can turn into a real business.

{kind=link}